Granular Panda

Reading the tea leaves on the pre-announced Google "helpful content" update rolling out next week & over the next couple weeks in the English language, it sounds like a second and perhaps more granular version of Panda which can take in additional signals, including how unique the page level content is & the language structure on the pages.

Like Panda, the algorithm will update periodically across time & impact websites on a sitewide basis.

Cold Hot Takes

The update hasn't even rolled out yet, but I have seen some write ups which conclude with telling people to use an on-page SEO tool, tweets where people complained about low end affiliate marketing, and gems like a guide suggesting empathy is important yet it has multiple links on how to do x or y "at scale."

Trashing affiliates is a great sales angle for enterprise SEO consultants since the successful indy affiliate often knows more about SEO than they do, the successful affiliate would never become their client, and the corporation that is getting their asses handed to them by an affiliate would like to think this person has the key to re-balance the market in their own favor.

My favorite pre-analysis was a person who specialized in ghostwriting books for CEOs Tweeting that SEO has made the web too inauthentic and too corporate. That guy earned a star & a warm spot in my heart.

Profitable Publishing

Of course everything in publishing is trade offs. That is why CEOs hire ghostwriters to write books for them, hire book launch specialists to manipulate the best seller lists, or even write messaging books in the first place. To some Dan Price was a hero advocating for greater equality and human dignity. To others he was a sort of male feminist superhero, with all the Harvey Weinstein that typically entails.

Anyone who has done 100 interviews with journalists see ones that do their job by the book and aim to inform their readers to the best of their abilities (my experiences with the Wall Street Journal & PBS were aligned with this sort of ideal) and then total hatchet jobs where a journalist plants a quote they want & that they said, that they then attributes it to you (e.g. London Times freelance journalist).

There are many dimensions to publishing:

- depth

- purpose

- timing

- audience

- language

- experience

- format

- passion

- uniqueness

- frequency

Blogs to Feeds

For a long time indy blogs punched well above their weight due to the incestuous nature of cross-referencing each other, the speed of publishing when breaking news, and how easy feed readers made it to subscribe to your favorite blogs. Google Reader then ate the feed reader market & shut down. And many bloggers who had unique things to say eventually started to repeat themselves. Or their passions & interests changed. Or their market niche disappeared as markets moved on. Starting over is hard & staying current after the passion fades is difficult. Plus if you were rather successful it is easy to become self absorbed and/or lose the hunger and drive that initially made you successful.

Around the same time blogs started sliding people spent more and more time on various social networks which hyper-optimized the slot machine type dopamine rush people get from refreshing the feed. Social media largely replaced blogs, while legacy media publishers got faster at putting out incomplete news stories to be updated as they gather more news. TikTok is an obvious destination point for that dopamine rush - billions of short pieces of content which can be consumed quickly and shared - where the user engagement metrics for each user are tracked and aggregated across each snippet of media to drive further distribution.

Burnout & Changing Priorities

I know one of the reasons I blog less than I used to is a lot of the things I would write would be repeats. Another big reason was when my wife was pregnant I decided to shut down our membership site so I could take my wife for a decently long walk almost everyday so her health was great when it came time to give birth & ensure I had spare capacity for if anything went wrong with the pregnancy process. As a kid my dad was only around much for a few summers and I wanted to be better than that for my kid.

The other reason I cut back on blogging is at some point search went from a endless blue water market to a zero sum game to a negative sum game (as ad clicks displaced organic clicks). And in such an environment if you have a sustainable competitive advantage it is best to lean into it yourself as hard as you can rather than sharing it with others. Like when we had an office here our link builders I trained were getting awesome unpaid links from high-trust sources for what backed out to about $25 of labor time (and no more than double that after factoring in office equipment, rent, etc.).

If I share that script / process on the blog publicly I would move the economics against myself. At the end of the day business is margins, strategy, market, and efficiency. Any market worth being in is going to have competition, so you need to have some efficiency or strategic differentiators if you are going to have sustainable profit margins. I've paid others many multiples of that for link building for many years back when links were the primary thing driving rankings.

I don't know the business model where sharing the above script earns more than it costs. Does one launch a Substack priced at like $500 or $1,000 a month where they offer a detailed guide a month? How many people adopt the script before the response rates fall & it offsets the costs by more than the revenues? My issue with consulting is I always wanted to over-deliver for clients & always ended up selling myself short when compared to publishing, so I just stick with a few great clients and a bit of this and that vs going too deep & scaling up there. Plus I had friends who went big and then some of their clients who were acquired had the acquirer brag about the SEO, that lead to a penalty, then the acquirer of the client threw the SEO under the bus and had their business torched.

When you have a kid seeing them learn and seeing wonderment in their eyes is as good as life gets, but if you undermine your profit margins you'd also be directly undermining your own child's future ... often to help people who may not even like you anyhow. That is ultimately self defeating as it gets, particularly as politics grow more polarized & many begin to view retribution as a core function of government.

I believe there are no limits to the retributive and malicious use of taxation as a political weapon. I believe there are no limits to the retributive and malicious use of spending as a political reward.

Margins

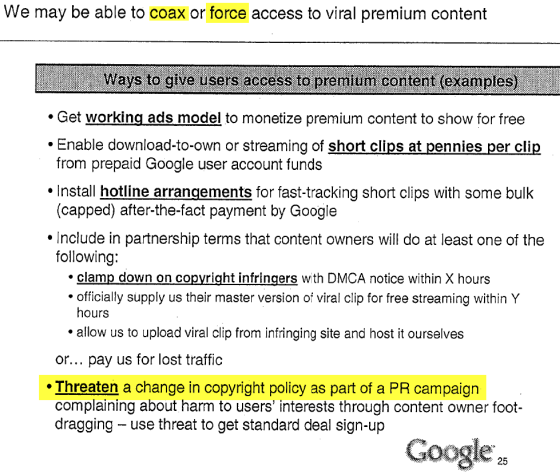

The role of search engines is to suck as much of the margins as they can out of publishing while trying to put some baseline floor on content quality so that people would still prefer to use a search engine rather than some other reference resource. Google sees memes like "add Reddit to the end of your search for real content" as an attack on their own brand. Google needs periodic large shake ups to reaffirm their importance, maintain narrative control around innovation, and to shake out players with excessive profit margins who were too well aligned with the current local maxima. Google needs aggressive SEO efforts with large profits to have an "or else" career risk to them to help reign in such efforts.

You can see the intent for career risk in how the algorithm will wait months to clear the flag:

Google said the helpful content update system is automated, regularly evaluating content. So the algorithm is constantly looking at your content and assigning scores to it. But that does not mean, that if you fix your content today, your site will recover tomorrow. Google told me there is this validation period, a waiting period, for Google to trust that you really are committed to updating your content and not just updating it today, Google then ranks you better and then you put your content back to the way it was. Google needs you to prove, over several months - yes - several months - that your content is actually helpful in the long run.

If you thought a site were quality, had some issues, the issues were cleaned up, and you were still going to wait to rank it appropriately ... the sole and explicit purpose of that delay is career risk to others to prevent them flying to close to the sun - to drive self regulation out of fear.

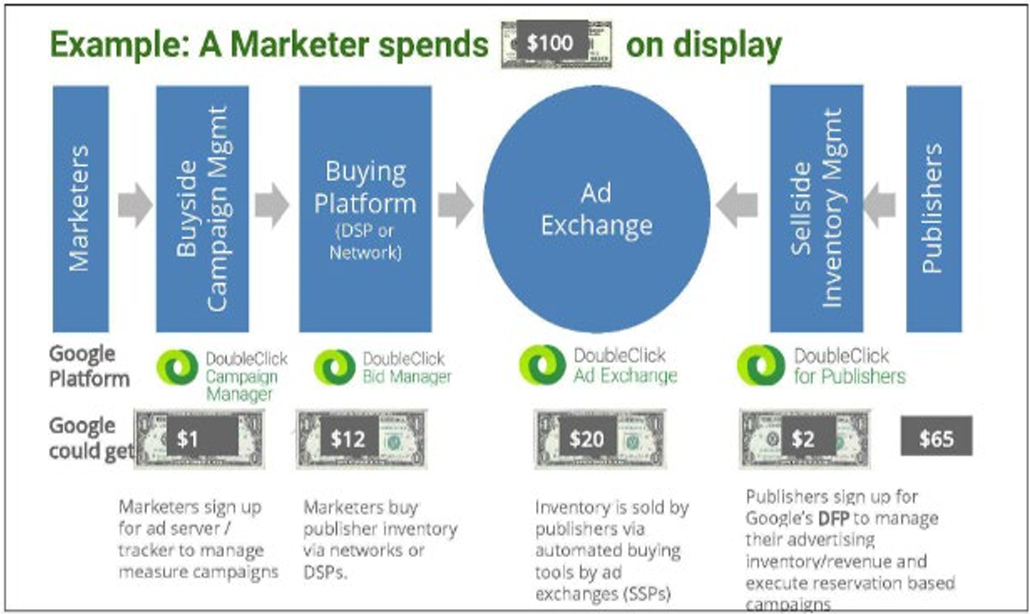

Brand counts for a lot in search & so does buying the default placement position - look at how much Google pays Apple to not compete in search, or look at how Google had that illegal ad auction bid rigging gentleman's agreement with Facebook to not compete with a header bidding solution so Google could maintain their outsized profit margins on ad serving on third party websites.

Business ultimately is competition. Does Google serve your ads? What are the prices charged to players on each side of each auction & how much rake can the auctioneer capture for themselves?

The Auctioneer's Shill Bid - Google Halverez (beta)

That is why we see Google embedding more features directly in their search results where they force rank their vertical listings above the organic listings. Their vertical ads are almost always placed above organics & below the text AdWords ads. Such vertical results could be thought of as a category-based shill bid to try to drive attention back upward, or move traffic into a parallel page where there is another chance to show more ads.

This post stated:

Google runs its search engine partly on its internally developed Cloud TPU chips. The chips, which the company also makes available to other organizations through its cloud platform, are specifically optimized for artificial intelligence workloads. Google’s newest Cloud TPU can provide up to 275 teraflops of performance, which is equivalent to 275 trillion computing operations per second.

Now that computing power can be run across:

- millions of books Google has indexed

- particular publishers Google considers "above board" like Reuters, AP, the New York Times, the Wall Street Journal, etc.

- historically archived content from trusted publishers before "optimizing for search" was actually a thing

... and model language usage versus modeling the language usage of publishers known to have weak engagement / satisfaction metrics.

Low end outsourced content & almost good enough AI content will likely tank. Similarly textually unique content which says nothing original or is just slapped together will likely get downranked as well.

Expect Volatility

They would not have pre-announced the update & gave some people some embargoed exclusives unless there was going to be a lot of volatility. As typical with the bigger updates, they will almost certainly roll out multiple other updates sandwiched together to help obfuscate what signals they are using & misdirect people reading too much in the winners and losers lists.

Here are some questions Google asked:

- Do you have an existing or intended audience for your business or site that would find the content useful if they came directly to you?

- Does your content clearly demonstrate first-hand expertise and a depth of knowledge (for example, expertise that comes from having actually used a product or service, or visiting a place)?

- Does your site have a primary purpose or focus?

- After reading your content, will someone leave feeling they’ve learned enough about a topic to help achieve their goal?

- Will someone reading your content leave feeling like they’ve had a satisfying experience?

- Are you keeping in mind our guidance for core updates and for product reviews?

As a person who has ... erm ... put a thumb on the scale for a couple decades now, one can feel the algorithmic signals approximated by the above questions.

To the above questions they added:

- Is the content primarily to attract people from search engines, rather than made for humans?

- Are you producing lots of content on different topics in hopes that some of it might perform well in search results?

- Are you using extensive automation to produce content on many topics?

- Are you mainly summarizing what others have to say without adding much value?

- Are you writing about things simply because they seem trending and not because you'd write about them otherwise for your existing audience?

- Does your content leave readers feeling like they need to search again to get better information from other sources?

- Are you writing to a particular word count because you've heard or read that Google has a preferred word count? (No, we don't).

- Did you decide to enter some niche topic area without any real expertise, but instead mainly because you thought you'd get search traffic?

- Does your content promise to answer a question that actually has no answer, such as suggesting there's a release date for a product, movie, or TV show when one isn't confirmed?

Some of those indicate where Google believes the boundaries of their own role as a publisher are & that you should stay out of their lane. :D

Barrier to Entry vs Personality

One of the interesting things about the broader scope of algorithm shifts is each thing that makes the algorithms more complex, increases barrier to entry, and increases cost ultimately increases the chunk size of competition. And when that is done what is happening is the macroparasite is being preference over the microparasite. Conceptually Google has a lot of reasons to have that bias or preference:

- fewer entities to police (lower cost)

- more data to use to police each entity (higher confidence)

- easier to do direct deals with players which can move the needle (more scale)

- if markets get too consolidated Google can always launch a vertical service & tip the scale back in the other direction (I see your Amazon ad revenue and I raise you free product listing ads, aggregated third party reviews, in-SERP product comparison features, and a "People Also Ask" unit)

- the macroparasites have more "sameness" between them (making it easier for Google to create a competitive clone or copy)

So long as Google maintains a monopoly on web search the bias toward macroparasites works for them. It gives Google the outsized margins which ensures healthy Alphabet profit margins even if the median of Google's 156,000+ employees pulls down nearly $300,000 a year. People can not see what has no distribution, people do not know what exist in invisibility, nor do they know which innovations were held back and what does not exist due to the current incentive structures in our monopoly-controlled publishing ecosystem.

I think when people complain about the web being inauthentic what they are really complaining about is the algorithmic choices & publishing shifts that did away with the indy blogs and replaced them with the dopamine feed viral tricks and the same big box scaled players which operate multiple parallel sites to where you are getting the same machinery and content production house behind multiple consecutive listings. They are complaining about the efforts to snuff out the microparasite also scrubbing away personality, joy, love, quirkiness, weirdness, and the zany stuff you would not typically find on content by factory order websites.

Let's Go With Consensus Here!

The above leads you down well worn paths, rather than the magic of serendipity & a personality worn on your sleeve that turns some people on while turning other people off.

Text which is roughly aligned with a backward looking consensus rather than at the forefront of a field.

History is written by the victors. Consensus is politically driven, backward looking, and has key messages memory holed.

Some COVID-19 Fun to "Fact" Check

I spent new years in China before the COVID-19 crisis hit & got sick when I got back. I used so much caffeine the day I moved over a half dozen computers between office buildings while sick. I week later when news on Twitter started leaking of the COVID-19 crisis hit I thought wow this looks even worse than what I just had. In the fullness of time I think I had it before it was a crisis. Everyone in my family got sick and multiple people from the office. Then that COVID-19 crisis news came out & only later when it was showed that comorbidities and the elderly had the worse outcomes did I realize they were likely the same. Then after the crisis had been announced someone else from the office building I was in got it & then one day it was illegal to go into the office. The lockdown where I lived was longer than the original lockdown in Wuhan. Those lockdowns destroyed millions of lives.

The reason the response to the COVID-19 virus was so extreme was huge parts of politically interested parties wanted to stop at nothing to see orange man ejected from the White House. So early on when he blocked flights from China you had prominent people in political circles calling him xenophobic, and then the head of public health in New York City was telling you it was safe to ride the subway and go about your ordinary daily life. That turned out to be deadly partisan hackery & ignorance pitched as enlightenment, leading to her resignation.

Then the virus spreads wildly as one would expect it to. And draconian lockdowns to tank the economy to ensure orange man was gone, mail in voting was widespread, and the election was secured.

Some of the most ridiculous heroes during this period wrote books about being a hero. Andrew "killer" Cuomo had time to write his "did you ever know that I'm your hero" book while he simultaneously ordered senior living homes to take in COVID-19 positive patients. Due to fecal-oral transmission and poor health outcomes for senior citizens sick enough to be in a senior living home his policies lead to the manslaughter of thousands of senior citizens.

You couldn't go to a funeral and say goodbye because you might kill someone else's grandma, but if you were marching for social justice (and ONLY social justice) that stuff was immune to the virus.

Suggesting looking at the root problems like no dad in the home is considered sexist, racist, or both. Meanwhile social justice organizations champion tearing down the nuclear family in spite of the fact that if you tear down the family all you are left with is the collective AND "mandatory collectivism has ended in misery wherever it’s been tried."

Of course the social justice stuff embeds the false narrative of victimhood, which then turns many of the fake victims into monsters who destroy the lives of others - but we are all in this together.

Absolutely nobody could have predicted the rise of murder & violent crime as we emptied the prisons & decriminalized large swaths of the penal code. Plus since many crimes are repeatedly ignored people stop reporting lesser crimes, so the New York Times can tell you not to worry overall crime is down.

In Seattle if someone rapes you the police probably won't even take a report to investigate it unless (in some cases?) you are a child. What are police protecting society from if rape is a freebie that doesn't really matter? Why pay taxes or have government at all?

What Google Wants

The above sidebar is the sort of content Google would not want to rank in their search results. :D

They want to rank text which is perhaps factually correct (even if it intentionally omits the sort of stuff included above), and maybe even current and informed, but done in such a way where you do not feel you know the author the way you might think you do if you read a great novel. Or hard biased content which purports to support some view and narrative, but is ultimately all just an act, where everything which could be of substance is ultimately subsumed by sales & marketing.

The Market for Something to Believe In is Infinite

Each re-representation mash-up of content in the search results decontextualizes the in-depth experience & passion we crave. Each same "big box" content factory where a backed entity can withstand algorithmic volatility & buy up other publishers to carry learnings across to establish (and monetize) a consensus creates more of a bland sameness.

That barrier to entry & bland sameness is likely part of the reason the recent growth of Substack, which sort of acts just like a blog did 15 or 20 years ago - you go direct to the source without all the layers of intermediaries & dumbing down you get as a side effect of the scaled & polished publishing process.