Google Rethinking Payday Loans & Doorway Pages?

Nov 12, 2013 WSJ: Google Ventures Backs LendUp to Rethink Payday Loans

Google Ventures Partner Blake Byers joined LendUp’s board of directors with his firm’s investment. The investor said he expects LendUp to make short-term lending reasonable and favorable for the “80 million people banks won’t give credit cards to,” and help reshape what had been “a pretty terrible industry.”

What sort of strategy is helping to drive that industry transformation?

How about doorway pages.

That in spite of last year Google going out of their way to say they were going to kill those sorts of strategies.

March 16, 2015 Google To Launch New Doorway Page Penalty Algorithm

Google does not want to rank doorway pages in their search results. The purpose behind many of these doorway pages is to maximize their search footprint by creating pages both externally on the web or internally on their existing web site, with the goal of ranking multiple pages in the search results, all leading to the same destination.

These sorts of doorway pages are still live to this day.

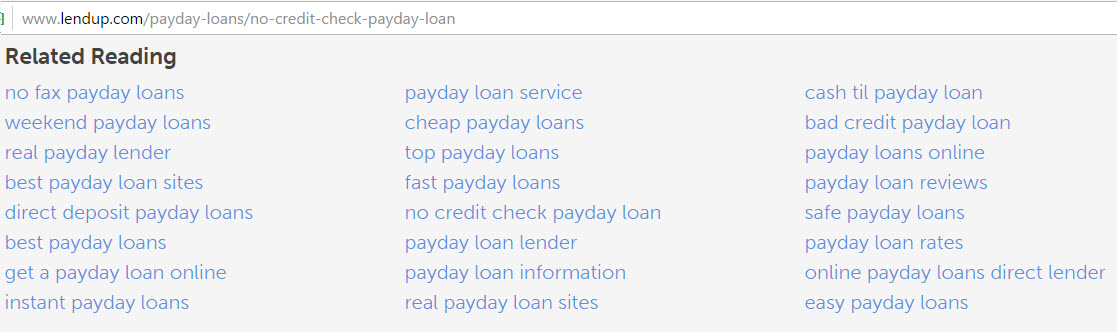

Simply look at the footer area of lendup.com/payday-loans

But the pages existing doesn't mean they rank.

For that let's head over to SEMrush and search for LendUp.com

Hot damn, they rank for about 10,000 "payday" keywords.

And you know their search traffic is only going to increase now that competitors are getting scrubbed from the marketplace.

Today we get journalists conduits for Google's public relations efforts writing headlines like: Google: Payday Loans Are Too Harmful to Advertise.

Today those sorts of stories are literally everywhere.

Tomorrow the story will be over.

And when it is.

Precisely zero journalists will have covered the above contrasting behaviors.

As they weren't in the press release.

Best yet, not only does Google maintain their investment in payday loans via LendUp, but there is also a bubble in the personal loans space, so Google will be able to show effectively the same ads for effectively the same service & by the time the P2P loan bubble pops some of the payday lenders will have followed LendUp's lead in re-branding their offers as being something else in name.

A user comment on Google's announcement blog post gets right to the point...

Are you disgusted by Google's backing of LendUp, which lends money at rates of ~ 395% for short periods of time? Check it out. GV (formerly known as Google Ventures) has an investment in LendUp. They currently hold that position.

Oh, the former CIO and VP of Engineering of Google is the CEO of Zest Finance and Zest Cash. Zest Cash lends at an APR of 390%.

Meanwhile, off to revolutionize the next industry by claiming everyone else is greedy and scummy and there is a wholesome way to do the same thing leveraging new technology, when in reality the primary difference between the business models is simply a thin veneer of tech utopian PR misinformation.

Don't expect to see a link to this blog post on TechCrunch.

There you'll read some hard-hitting cutting edge tech news like:

Banks are so greedy that LendUp can undercut them, help people avoid debt, and still make a profit on its payday loans and credit card.

#MomentOfZeroTruth #ZMOT

Update: Kudos to the Google Public Relations team, as it turns out the CFPB is clamping down on payday lenders, so all the positive PR Google got on this front was simply them front running a known regulatory issue in the near future & turning it into a public relations bonanza. Further, absolutely NOBODY (other than the above post) mentioned the doorway page issue, which remains in place to this day & is driving fantastic rankings for their LendUp investment.

Update 2: Record keeping requirements do not improve things if a company still intentionally violates the rules, knowing they will only have to pay a token slap on the wrist fine if and when they are finally caught. All it really does is drive the local businesses under.

The massive record-keeping and data requirements that Mr. Corday is foisting on the industry will have another effect: It will drive out the small, local players who have dominated the industry in favor of big firms and consolidators who can afford the regulatory overhead. It will also favor companies that can substitute big data for local knowledge like LendUp, the Google-backed venture that issued a statement Thursday applauding the CFPB rules. Google’s self-interest has become a recurrent theme in Obama policy making

Those records (along with the Google duplicity on doorway pages) however confirm that LendUp are not the good guys! They were outright scamming & over-charing their customers:

Onine lending start-up LendUp, which has billed itself as a better and more affordable alternative to traditional payday lenders, will pay $6.3 million in refunds and penalties after regulators uncovered widespread rule-breaking at the company.

Update 3: The CFPB repeatedly sued LendUp for military lending act violations & violating a 2016 consent order by continuing to use illegal and deceptive marketing.

“LendUp lures consumers with false promises that repeat borrowing would allow them to ‘climb the LendUp Ladder’ and unlock lower interest rates. For tens of thousands of borrowers, the LendUp Ladder was a lie,” said CFPB Acting Director Dave Uejio. “Not only did LendUp structure its business around wholesale deception and keeping borrowers in cycles of debt, the company doubled down after getting caught the first time. We will not tolerate this illegal scheme or allow this company to continue preying on vulnerable consumers.”

LendUp's repeat criminal conduct was so absurd the CFPB forced the company to shutter.

Comments

I want to thank Google for this! First, I'll make some serious cash on my ENOVA shares because they've been lending since 1998 and built a huge data base of borrowers. With this latest Big Brother implementation by Google, ENOVA's data base will seriously increase in value. Second, my payday loan stores and those of my clients will experience increased valuations by attracting brick-n-mortar borrowers. This action by Google does ZERO for loan demand. It simply blows up the sophisticated lead gen guys and sends more advertising to Bing. Facebook left payday loan ads out to dry long ago. Payday loans, cannabis, guns... sure is nice to know the majority of us have no clue what's best for us and have the 1% watching our backs.

"This action by Google does ZERO for loan demand. It simply blows up the sophisticated lead gen guys and sends more advertising to Bing."

And that was part of what I was trying to highlight by bringing up LendUp. They are simply re-routing traffic and monetizing it by other means.

Of course companies like Wonga or such which have a great organic ranking will get even more traffic, but in US perhaps the company with the biggest organic ranking footprint in that category is one they are invested in. - LendUp

You can look at Google's aggregate broad match downstream traffic by keyword using tools like Compete.com & for 'payday loan' only AceCashExpress.com had a significant lead on LendUp. And big chunks of that lead are likely driven by the combination of local results from having their physical locations & perhaps advertising more aggressively.

Also if in the future they shift local results to pay-to-play AND are refusing cash from payday lenders, then that would mean someone like Ace Cash Express might not be able to rank locally. Between stripping away that channel and AdWords one could conceivably see LendUp getting over 10% of the online market without having to own any physical retail stores or such.

I was just looking at Lendup the other day. They must have been penalized because the homepage wasn't even ranking for their brand name. You can see a small drop the past two months in SEMrush. They're back already so it must have been a short penalty. Pretty sad since their rankings look like their based on an XRumer blast. Just another slap on the wrist for Google Ventures backed companies.

...after all, in some cases those sorts of links are from competitors. And/or perhaps they have been disavowed.

But they also have long standing doorway pages that rank great to this day. And those doorway pages were published before Google warned against the practice last year & those doorway pages still rank to this day.

You realize that Google not allowing payday loan sites to advertise has nothing to do with organic SEO, right? And you realize that LendUp is going to get hit with that too, right?

Stop with this conspiracy theory garbage.

.... If a company claims to be taking a moral stance against a product or service they should divest in any stake they have in companies in that field.

Either the move is one based on moral beliefs and they are unaware of their investments in the category, or the sudden moral change after all these years is based on running the numbers ...

+ lift in PR value perception

- loss in revenue from payday ads

+ gain in value of investment in category

+ revenue from personal loan bubble to offset some of the loss in payday ad revenue

There is no conspiracy garbage in highlighting Google remains invested in the category & their investment has a long standing policy of violating Google's webmaster guidelines to gain a competitive edge.

Those are facts of the matter.

What makes the doorway pages even more insulting (to someone like one of my buddies who got clobbered by Google years ago) is...

You don't have to believe my take on this. Just look at the DOZENS of "payday loan" themed doorway pages published by LendUp. That is them telling you what they think they are relevant for & what they are trying to rank for & how they are trying to position their product.

Adding the word "alternative" somewhere on the page still doesn't change the fact they are essentially selling the same thing.

Every niche has companies who don't play by the rules, payday loans industry just has more of them than average, but this does not mean that everyone should be punished. There is a reason why people are searching for payday loans, taking away the paid listing doesn't help them for sure since it doesn't fix the problem.

Larry Clement from loanscanadaonline.com

Aaron, keep fighting the good fight, owning both the platform and then making strategic investments in key businesses that operate under a double standard (thumbtack) needs a serious media outlet to start shining the light into how manipulative for $ the good folks at Google really are.

Add new comment